We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

ASML Surges 36% in 3 Months: Should Investors Buy the Stock?

Read MoreHide Full Article

Key Takeaways

ASML shares rose 36.3% in three months, outperforming the industry, sector and S&P 500.

AI data centers and hyperscale computing are fueling demand for ASML's advanced lithography systems.

ASML expects 2026 net sales of Euro 36B-40B, with gross margin between 51% and 53%.

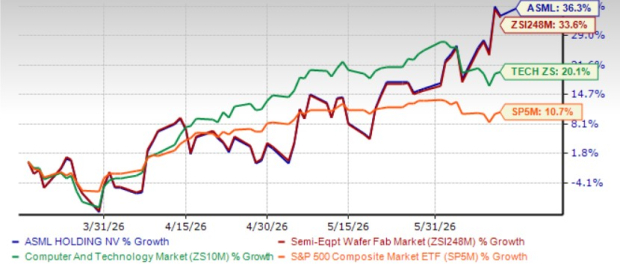

Shares of ASML Holding (ASML - Free Report) have gained 36.3% in the past three months, outperforming the industry, its sector as well as the Zacks S&P 500 composite in the same time frame. ASML shares are trading at a discount to their 52-week high.

ASML Holding is a critical player in the global semiconductor industry, maintaining a dominant position in extreme ultraviolet (EUV) lithography systems. Industry prospects remain strong, fueled by rising AI-driven infrastructure spending that is boosting demand for advanced logic and memory chips. Supported by its comprehensive product portfolio, management expects robust Memorychips across all business segments.

ASML vs Industry, Sector, S&P 500 in 3 Months

Image Source: Zacks Investment Research

Shares of KLA Corporation (KLAC - Free Report) and Applied Materials (AMAT - Free Report) have rallied 73.1% and 66.2% in the past three months, respectively.

ASML Shares Are Expensive

The stock is overvalued compared with its industry. It is currently trading at a price-to-earnings multiple of 44.34, higher than the industry average of 43.63 and the median of 32.65 over the past three years. It has a Value Score of F.

Image Source: Zacks Investment Research

ASML shares are more expensive than Applied Materials but cheaper than those of KLA Corporation.

The Case for ASML Stock

ASML continues to benefit from robust demand for its wafer fabrication equipment, driven by the increasing adoption of advanced semiconductors across AI data centers and hyperscale computing environments. Management expects favorable end-market trends to support a richer product mix, characterized by rising demand for advanced lithography systems and greater lithography intensity.

The company believes its broad and flexible portfolio positions it well to address evolving customer needs. Through the expansion of its holistic lithography solutions, support for 3D integration technologies, ongoing improvements in the performance and cost efficiency of both deep ultraviolet and EUV systems, and continued scaling of EUV technology over the coming decade, ASML aims to preserve its technological leadership.

Artificial intelligence remains a key long-term growth catalyst for the company. The increasing computational demands of AI applications require more advanced semiconductors, including cutting-edge GPUs and high-bandwidth memory chips, both of which rely heavily on EUV lithography for production. This trend is expected to drive sustained demand for ASML’s equipment in the years ahead.

Financially, ASML is supported by strong profitability and consistent cash generation. Its portfolio of high-value systems, recurring service revenues and extensive installed base contributes to stable margins and enhanced earnings visibility. Moreover, the company’s sizable order backlog provides solid visibility into future revenue growth.

ASML also remains focused on returning value to shareholders through a growing dividend and ongoing share repurchase initiatives. However, competitive risks persist. A growing number of companies are entering the semiconductor equipment market, particularly in etching solutions, and are winning contracts by leveraging their specialized technological capabilities and expertise.

ASML’s Growth Prospects Solid

The Zacks Consensus Estimate for fiscal 2026 and 2027 revenues indicates a 22.6% and 24.8% increase year over year, respectively.

The consensus estimate for fiscal 2026 and 2027 earnings implies a 31.9% and 34.6% year-over-year increase, respectively. The expected long-term earnings growth rate is pegged at 33.9%, better than the industry of 32%.

ASML expects second-quarter 2026 total net sales between €8.4 billion and €9.0 billion, and a gross margin between 51% and 52%.

ASML estimates 2026 total net sales to be between €36 billion and €40 billion, with a gross margin between 51% and 53%.

Over the long run, ASML envisions achieving 2030 annual revenues between approximately €44 billion and €60 billion, with a gross margin between approximately 56% and 60%.

Mixed Analyst Sentiment on ASML

The consensus estimate for 2026 earnings has moved 0.6% south in the last 30 days, while that for 2027 moved 3.2% north.

Image Source: Zacks Investment Research

The consensus estimate for KLA Corporation’s 2026 and 2027 earnings witnessed no movement in the last 30 days.

The consensus estimate for Applied Materials’ 2026 and 2027 earnings has moved north in the last 30 days.

Parting Thoughts on ASML Shares

ASML remains well-positioned for future growth, underpinned by its dominant leadership in EUV lithography and a robust order backlog. Secular demand drivers such as AI, cloud computing, and advanced semiconductor manufacturing continue to support its long-term outlook, while favorable analyst sentiment further reinforces confidence in the company’s growth prospects.

Image: Bigstock

ASML Surges 36% in 3 Months: Should Investors Buy the Stock?

Key Takeaways

Shares of ASML Holding (ASML - Free Report) have gained 36.3% in the past three months, outperforming the industry, its sector as well as the Zacks S&P 500 composite in the same time frame. ASML shares are trading at a discount to their 52-week high.

ASML Holding is a critical player in the global semiconductor industry, maintaining a dominant position in extreme ultraviolet (EUV) lithography systems. Industry prospects remain strong, fueled by rising AI-driven infrastructure spending that is boosting demand for advanced logic and memory chips. Supported by its comprehensive product portfolio, management expects robust Memorychips across all business segments.

ASML vs Industry, Sector, S&P 500 in 3 Months

Image Source: Zacks Investment Research

Shares of KLA Corporation (KLAC - Free Report) and Applied Materials (AMAT - Free Report) have rallied 73.1% and 66.2% in the past three months, respectively.

ASML Shares Are Expensive

The stock is overvalued compared with its industry. It is currently trading at a price-to-earnings multiple of 44.34, higher than the industry average of 43.63 and the median of 32.65 over the past three years. It has a Value Score of F.

Image Source: Zacks Investment Research

ASML shares are more expensive than Applied Materials but cheaper than those of KLA Corporation.

The Case for ASML Stock

ASML continues to benefit from robust demand for its wafer fabrication equipment, driven by the increasing adoption of advanced semiconductors across AI data centers and hyperscale computing environments. Management expects favorable end-market trends to support a richer product mix, characterized by rising demand for advanced lithography systems and greater lithography intensity.

The company believes its broad and flexible portfolio positions it well to address evolving customer needs. Through the expansion of its holistic lithography solutions, support for 3D integration technologies, ongoing improvements in the performance and cost efficiency of both deep ultraviolet and EUV systems, and continued scaling of EUV technology over the coming decade, ASML aims to preserve its technological leadership.

Artificial intelligence remains a key long-term growth catalyst for the company. The increasing computational demands of AI applications require more advanced semiconductors, including cutting-edge GPUs and high-bandwidth memory chips, both of which rely heavily on EUV lithography for production. This trend is expected to drive sustained demand for ASML’s equipment in the years ahead.

Financially, ASML is supported by strong profitability and consistent cash generation. Its portfolio of high-value systems, recurring service revenues and extensive installed base contributes to stable margins and enhanced earnings visibility. Moreover, the company’s sizable order backlog provides solid visibility into future revenue growth.

ASML also remains focused on returning value to shareholders through a growing dividend and ongoing share repurchase initiatives.

However, competitive risks persist. A growing number of companies are entering the semiconductor equipment market, particularly in etching solutions, and are winning contracts by leveraging their specialized technological capabilities and expertise.

ASML’s Growth Prospects Solid

The Zacks Consensus Estimate for fiscal 2026 and 2027 revenues indicates a 22.6% and 24.8% increase year over year, respectively.

The consensus estimate for fiscal 2026 and 2027 earnings implies a 31.9% and 34.6% year-over-year increase, respectively. The expected long-term earnings growth rate is pegged at 33.9%, better than the industry of 32%.

ASML expects second-quarter 2026 total net sales between €8.4 billion and €9.0 billion, and a gross margin between 51% and 52%.

ASML estimates 2026 total net sales to be between €36 billion and €40 billion, with a gross margin between 51% and 53%.

Over the long run, ASML envisions achieving 2030 annual revenues between approximately €44 billion and €60 billion, with a gross margin between approximately 56% and 60%.

Mixed Analyst Sentiment on ASML

The consensus estimate for 2026 earnings has moved 0.6% south in the last 30 days, while that for 2027 moved 3.2% north.

Image Source: Zacks Investment Research

The consensus estimate for KLA Corporation’s 2026 and 2027 earnings witnessed no movement in the last 30 days.

The consensus estimate for Applied Materials’ 2026 and 2027 earnings has moved north in the last 30 days.

Parting Thoughts on ASML Shares

ASML remains well-positioned for future growth, underpinned by its dominant leadership in EUV lithography and a robust order backlog. Secular demand drivers such as AI, cloud computing, and advanced semiconductor manufacturing continue to support its long-term outlook, while favorable analyst sentiment further reinforces confidence in the company’s growth prospects.

Given a premium valuation and mixed analyst sentiment, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) stock now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.